22 Nov Inflation: How Did We Get Here and What Should Investors Do? – Podcast

In today’s episode Nicholas Ryder, CFA® joins Nicholas Olesen, CFP®, CPWA® to talk about one of the hottest topics in the news, inflation. He shares both how and why inflation has been rising quite a bit recently and also what, if anything, investors should do about it.

This timely episode comes just a week after the latest reading of inflation came in at over 6% year-over-year, the highest value since the 90’s. We have been receiving many questions from listeners and clients asking what our view of and what they can do about inflation. This episode covers:

- Quick background on how inflation is measured

- How and which policy responses to COVID brought on much of this

- Why the recent surge in inflation

- His outlook for inflation

- What investors can and should do about inflation

You can find a transcript of today’s show below and the charts referenced in the episode.

To listen to all our episodes and receive them as we publish, please subscribe to our podcast on your favorite app:

![]()

![]()

![]()

![]()

Please send us feedback and any topic or questions you would like us to cover. Email us at: [email protected]

Chart referenced:

Transcript from today’s show:

[00:00:19] Nicholas Olesen: Thanks for tuning into A Wealth of Advice. My name is Nicholas Olesen, Director of Private Wealth at Kathmere Capital. Today we want to touch on inflation. I’m sure you guys have all read about it, heard about it, seen all the headlines coming across. And so today we’re joined with Nick Ryder, Chief Investment Officer here at Kathmere, and he’s going to go over just some of the biggest questions we’ve gotten from clients about inflation.

So welcome to the podcast again.

[00:00:42] Nicholas Ryder: Thanks for having me always great to be here.

[00:00:44] Nicholas Olesen: Always fun.

So let’s start off with the broad question. What’s going on with inflation?

[00:00:50] Nicholas Ryder: Yeah. So right when we’re talking about inflation it’s in my perspective, um, general increase of the, of the price level of goods and services that we all buy. And so most commonly, um, used metric or proxy to measure inflation, what’s called the consumer price index or CPI for short. Um, and that’s just a weighted average basket of goods and services purchased by consumers around the country. So right. It includes food, clothing, shelter fuels, transportation costs, healthcare services, drugs, other goods and services. Right. Then. The CPI baskets, the weighted average of everybody in the economy. Obviously each of our individual purchase baskets are different. And so inflation for one person may feel very different than what’s being measured in the basket. But the baskets, what we have nonetheless.

And so why has inflation come back up as a topic?

Well, uh, we’re getting the highest readings we’ve seen in about three decades, um, right now in terms of year over year price changes. So just to put some numbers on it, um, The, the bureau of labor statistics just came out with, it’s a reading of CPI inflation in October of this year and on a year over year basis, the headline as it’s called number was up 6.2% from a year ago. That was the highest reading we’d seen on that since 1990.

Um, there’s another one that gets looked at and talked about a lot, which is called the core CPI. So that just strips out or excludes, um, very real, um, costs that we all pay, which is energy and, uh, food prices, but those tend to be volatile. So economic, you know, uh, Watchers tend to strip those out sometimes to try to get a better understanding of what’s really going on as the core name, so to speak. That was up 4.6% year from a year ago basis. That was also the highest reading in this case since early 1991. So, you know, your both, regardless of how you cut it, regardless how you look at inflation in terms of, uh, the price rise highest, highest we’ve seen now going back about 30 years. And so naturally that started to draw a lot of attention.

I I’d say the, you know, the other thing you’ll read in the paper or see on TV is, you know, what’s been so striking about this is, is we had been living in an era where inflation had been, you know, a non-issue so to speak. Um, it had always been around, uh, but inflation, uh, for really the last two decades now, we’ve been living in this period called kind of quote unquote, “the great moderation of inflation”, where inflation had been pretty persistently in the one to 2% per year.

[00:03:24] Nicholas Olesen: Yeah, because that was, I mean, that was the big fed policy was, Hey, we’re going to get inflation to 2%. That was like one of their mandates that they could talk to…

[00:03:31] Nicholas Ryder: That the fed and the monetary policy authorities, our objective has been, you know, this dual mandate of price, stability, and, um, promoting full employment and the price stability to them. They had defined that as, um, inflation at, or, you know, right around 2% per year. And, um, really coming out from. The global financial crisis of 2009, the fed hasn’t even able to get, get inflation near that two number. It’s constantly been somewhere one to 2%. So a lot of this chat, this focus was how do we push inflation back more towards our targeted two. Um, and keeping in mind all of this comes on on the heels, you know, the last 30 years is kind of great moderation where inflation has been very stable and under control, follows from the period of the much more tumultuous late 1960s into the early 1980s, where inflation was a very big problem, right? It was the zero kind of dubbed “The Great Inflation” where you had inflation in the seventies um, constantly above 5%. Um, I think for the decade average, somewhere in the high single digits, ultimately peaked out at 15%, almost in 1980, before Paul Volcker and the fed really took on this commitment to, to stifling off inflation. The medicine to do that was quite painful. And so a lot of people have these very painful memories of The Great Inflation Era, where, right, it was price spikes, commodity shortages, right. We all have seen the pictures or lived through the, you know, sitting in line, waiting for gas and, you know, being able to get gas based on, um, whether or not you had an odd and even number on the last, as the last digit of your license plate. Um, so the rationing and shortages that happen in. So, um, I think people are starting to have these fears that “are we headed back towards?”

[00:05:11] Nicholas Olesen: Yeah. And I think that like, that’s, that’s what we’re hearing from clients. That’s the main picture, if you will, that they’re painting, which just says, “I’m hearing about inflation. I remember, or I’ve heard stories about the 70’s into the 80’s. What does that mean?” And I think one of the things, when you dive into the inflation number, everyone kind of has their spins on it, but the CPI number for all the conversations that people have about not liking it. It’s a fair way of us gauging what inflation is, roughly.

What I’d love to do is just kind of say, okay, how did we get here? And then what’s behind this big surge?

And just to put it a context here, we’re recording this it’s mid- November 2021. So we are coming off of, or, or still in whatever you want to say, pandemic life, and I think a lot of people are blaming that, but I’d love to kinda hear your take on that.

[00:06:01] Nicholas Ryder: Yeah. I, I think it’s important again to remember this, that right. We’ve had this surge. We’re up at 6% year over year. And it’s just in such stark contrast to the lived experience really now for the last three decades for, for many of us, which has been the prime of our earning and spending years. Right. And so, um, naturally we’ve had kind of this shock to the system, so to speak that we’ve moved, um, you know, where we go from here, that’ll be, be the open question and we can certainly get into that. But, you know, let’s rewind and say, how do we get here? How do we get to the point where inflations, you know, 6% year over year?

Um, I think the short answer is, you know, in one word COVID. Um, now let’s elaborate on that a little more.

I, I think there’s this combined effect of the health crisis itself in then, you know, not making a value judgment or not debating the merits of some of this, but then it was the policy responses that followed the health crisis. And so the policy responses, you know, in terms of to control the spread of the virus and, you know, uh, promote public health as well as then to deal with the economic fallout of, of some of those actions.

But when we think about it, what’s kind of, again, at the highest macro level, Econ 101 type stuff here. Price of any good or service is going to be a function of two factors, right. The supply of that good. And the demand for that good. And so that all applied to individual goods and services, but then also you can think about that as applying at the, the, the aggregate level to, you know, the core price index, um, or the consumer price index.

And so, you know, to, to kind of summarize what’s what happened is right COVID plus the policy responses, have effectively resulted in this big surge in demand. Um, people have more money in their pockets and are spending it. And there’s this compositional effect, right? We’ve had some shifting from spending on services to goods as people haven’t been going out. Yup. Repairs to the home, making your home life better electronic, right? All of these things. So some shifting in the competition, but in aggregate demand, or the amount of money being spent is it’s pretty considerably up over the last now two years. And at the same time you’ve had supply, that’s been insufficient obviously to meet that demand and so you’ve seen pricing prices.

Depending what you’re looking at sometimes supply is still below 2019 baseline levels. Sometimes supply has expanded and either case supply hasn’t expanded enough to meet this surge in demand.

Yeah, we can go back and, you know, to put more minoosh on it. Right? Like, let’s talk about some of the details, right?

Policy response initially. We all go back now to the kind of what’s the dark days of March of 2020, right?

[00:08:40] Nicholas Olesen: Yep.

[00:08:41] Nicholas Ryder: Lock downs, restrictions on activity.

[00:08:43] Nicholas Olesen: Yep.

[00:08:44] Nicholas Ryder: So what happened there? Right? You had this kind of collapse in both demand, as well as supply. People couldn’t work. People couldn’t produce. People also couldn’t spend money on a lot of things.

So you had this drop. Well you had was, you know, the result of this all was government effectively took away people’s livelihood in order to promote public health. And again, not debating the merits, whether or not that was a right or wrong thing to do, uh, simply stating as a factor of what happened.

Resultingly or accordingly, the government said we’re taking away your livelihood, we’re now going to give you money to replace, you know, for most people, the income loss in, and many people actually saw their incomes expand as a result of all these economic stimulus activities. Right. We go back through the laundry list of these things.

There were three waves of direct stimulus checks, paid to people, you know, meeting income qualifications. You had the small business forgivable loans program, paycheck protection program, you had just cash payouts to, you know, economically critical businesses. You’ve seen expanded child tax care credits the expanded and enhanced unemployment benefits, right?

There’s a whole laundry list of things effectively. I think the government has now run up $5 trillion worth of deficits since the start of 2020. Right. That’s all money going out into, by and large consumers pockets. Um, you’ve had monetary policy essentially monetize that, so to speak. Issues treasury bonds to gain cash, to pay for it in the federal reserve was on the backend and buying those all up and creating new money, new dollars out of thin air effectively.

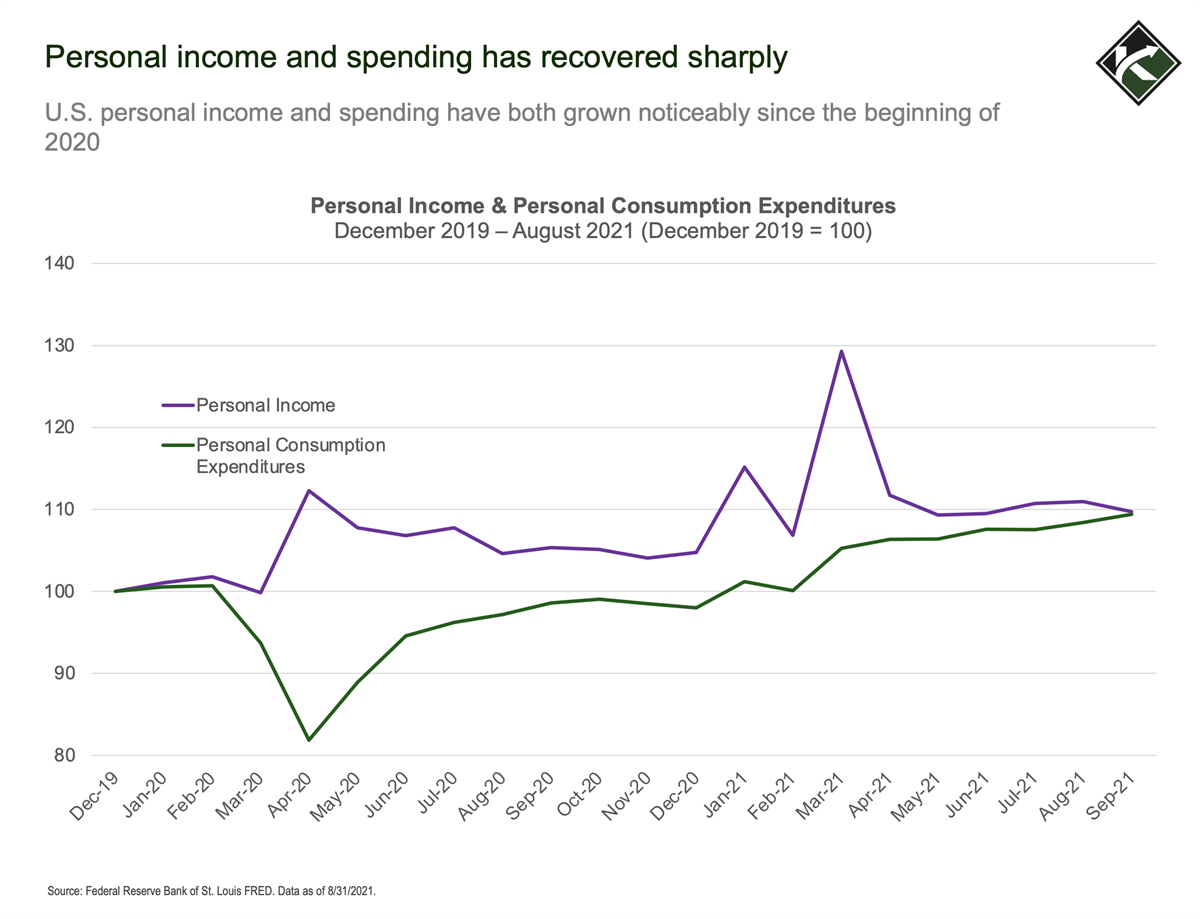

Yup. So right. You think about it. This, all this money showed up into the economy. Um, ultimately, you know, household income, we have this chart in our client review materials. It’s just, it’s fascinating to look at it. Just plots monthly income to households in the account. On a month-by-month basis relative to, uh, December of 2019 levels.

And you look at it and no recession has ever apparent in there, right? The line kind of slowly trends its way upward into the right there’s growth over the whole period. I think income is about 10% higher now on a monthly basis, anywhere it was. But you also in there have these three major spikes or kind of mountain peaks that happen.

And those all coincided with the three waves of stimulus. Right. Income state high earned income dropped a little bit in 2020, but not much. Um, and then you had these, you know, transfer payments happen to the extent that income in 2020 was higher than it was in 2019 and 2021. It’s going to be even higher yet.

So income was up, um, you had this surge in income, ultimately, eventually that led to kind of, uh, uh, uh, an increase in demand, right? Uh, people had money, they were willing, you know, in their pocket. Uh, and they spent it, um, and that, as I mentioned, composition, change more spending on goods a little bit less on services.

And at the same time, then, you know, you’ve had this supply, hasn’t been able to keep up with it on the good side. Um, it’s good. Supply has grown, but not enough. So you have this imbalance there on the services side, right? We’re not quite there, but demand is not quite where it was. There’s a little bit of imbalance, not nearly the same, uh, but the combined effect is you’ve just had prices go up to account.

[00:11:55] Nicholas Olesen: Yeah, I think we’ve all felt that in real life, whether it’s neighbors or ourselves. Like we did a little house project during the middle of all this. Everyone I talked to that’s a client, uh, is doing something to their house, staying in it for as long as they had. And so I think that goods side of it, you would hope at some point, the supply chain comes back. And I think that’s part of the question.

And we’re going to put in the show notes, I’ll put in that chart because it is a fascinating chart, the income side. And you see this drop down on what people spent, but income, you know, this huge gap between what people made, quote unquote, because of the stimulus now.

So let’s talk about that. So when you look at, then the surge now versus a year ago, why are we seeing this recent surge in inflation?

[00:12:35] Nicholas Ryder: Yeah, it’s it’s…

[00:12:38] Nicholas Olesen: Is it just kind of like, it just finally culminated to a fact that now we’re seeing it?

[00:12:43] Nicholas Ryder: Yeah. I mean, I think that’s probably a part of, you know, part of what’s now happening, and this is where go back to the spring and people were talking about, right, a lot of this whole debate has been, is inflation going to be transitory is kind of the word that’s been abandoned about, particularly in the policy policy-making circles.

And so you’ve had this surge recently part one of the things that came up with this debate is everybody kind of expected that inflation during the spring and early part of the summer would, would show high year over year comparisons and the, the re the reason on that being soft, so to speak year over year comparisons, right. Back in, um, March of 2020, April, May when, you know, economic shutdowns were happening, when people weren’t spending prices did dip.

And so then you look a year later when you make these year over year comparisons, they’re off of easy comparables. And so I think people expected, you know, we’re going to see inflation rise and you did see the numbers, um, numbers rise in the early part of, of this year, right? Like inflation numbers. Lat in this past April, we’re 4% year over year.

And we’ve kind of been in this four or five now increasing to six on a year over year. But so I think everybody expected that you would have this bump. I think the other side of it, what people were expecting to see was you will have some supply chain bottlenecks that are just a result of the fact that you kind of shut the economy off like a light switch a year ago and you’ve turned it on, but it hasn’t been perfectly synchronized.

Right? There’s very disparate reopening in different sectors. Within just the U S and then expand that out globally with supply chains, right? Other countries are still at different phases of reopening and have different levels of restriction. Right. And are, you know, at different phases of combating the virus.

And so I think people rightfully looked and said, yes, there are going to be all these kinks that are running to take time to work out. Um, the reality is too that the system got flooded with a lot of extra cash. Um, and so I think this combination of. Yeah. So for year over year comparisons, supply chain bottlenecks, right.

Everybody expected that we’d have some modicum of inflation and it’s just kind of continued to rise, um, in, in the last couple of months. And I think know some people are kind of saying, I told you so, and there’s others that continue to say. I believe this, you know, totally acknowledged that this is happening, but we continue to believe that like through time, this, these things will work themselves out and inflation will return more towards quote unquote normalized, call it 2% levels.

[00:15:17] Nicholas Olesen: Okay. So when we look at that and the biggest question we got, which is setting the stage, which you just did. Okay. How did we get here? But I think the bigger question and the more so what:

Where do we go from here? What’s your outlook? What do we do for inflation? How do you go about that going forward?

Because it makes it, it all makes sense how we got here. I think we all expected it. It was just the transitory term, which I’m glad you brought up because that’s been all over the place. But yeah, where did we go?

[00:15:48] Nicholas Ryder: Yeah.

And so again, it’s a, it’s a fantastic question. I don’t have a crystal ball. Nobody does. What I try to do is, you know, I try to listen to thoughtful people on this, try to form my own opinions. Um, what I’ve kind of done is take stock of, you know, What’s the case for inflation to be quote unquote transitory. Like what are the people saying? Why they believe that, Hey, yeah, we’re having this spike, but it’s going to come back down.

Um, what are the other people saying or making the case for? Ah, I, you know, I actually think higher inflation could be with us for. And importantly, right? Like there’s a couple of dimensions to this whole debate, which is what timeframe are you talking about? What magnitude of inflation, right? Like is, you know, it’s very different to say, I expect inflation to be sustained and remain with us.

And by that mean, it’s going to say at four to 6%, for a couple of years, That’s something entirely different, then we’re heading back to 1980 word peaked out at 15%. Those are two different things. It’s transitory. Yeah. We’re in this surge now, but I think by next summer, it’ll normalize or is it transitory for me to say it’s going to stay high for five years and then roll over, right?

Like, sure. Technically I guess the 1970s were transitory lasted for 10 years, but it did come down. Yeah. So. That’s all, you know, how I’ve kind of approaches, but, um, coming back to, you know, the main debate today is a trencher, not monetary makers, policymakers at the fed, um, in the, in the administration. And actually a lot of the large institutional asset management committee is all.

Pretty pretty gung-ho on, yes, we’re having this spike, but it will dissipate it normalize itself by call it next spring. Next summer expect to start seeing 2% or so inflation numbers. Um, you know, the general rationale behind that point of view is that it comes back to, we have these supply chain bottlenecks that are going to abate on their own as time passes that the recent surge is really as a result of this kind of shock to the economic system that came from COVID, uh, It’s related to the kind of, you know, unsynchronized reopening of the economy, right?

All of these things that are just going to work themselves out, um, that people will find a way to persist. Supply chains will adapt, adapt innovation, right? All these things we’ll work it out. And we’re going to find ourselves back at 2%, you know, next spring let’s say, um, And look, I think there’s probably a lot of truth to that.

I think there are certain elements of that. That certainly makes sense. I think some of the other arguments people will say that I find potentially compelling, why inflation is unlikely to remain elevated and sustained would be. Hey, we live in a world of incredible technology, enhancements and innovation, and that right as these things continue to happen, that has the natural result in driving the price of goods and services down through time.

Right? Like, just think about, you know, the computer sitting here on our table, our smartphones, these tablets, like absolutely remarkable what goes into those and that those, you know, those are accessible at the prices that, you know, Are pretty remarkable. Um, and so goods and services come down and we can drive efficiencies in the system and that’s not letting up anytime soon.

And as a result, right? Like goods and services are going to be delivered more cheaply and efficiently. And so inflation just isn’t likely to take, hold the way it did in the seventies or eighties, where it was a much more manufacturing, heavy, intensive economy where innovation wasn’t as great automation wasn’t as great.

It was all labor intensive. So. That’s one argument. Another one you hear a lot is, um, one of the main drivers of the seventies style inflation was you had a much more, uh, um, robust union membership around the world. And so collective bargaining was far stronger, both in the private and the public sector.

Um, they were able to negotiate cost of living, increases into wages, which then kind of created this wage price spiral where companies would see, I have to pay more. So I have to increase prices, you know, consumers of see I’m paying more. I need to drive more, you know? And so these things almost got themselves on autopilot, driving themselves higher.

Today, though union membership on the private sector, extreme, extremely low public sector. It’s still there, but you know, nevertheless far weaker than it was. And so that, that power of labor, so to speak, to drive wage increases, isn’t quite the same. You know, you starting to see some anecdotes of it. Right?

Dear John Deere, um, strike and resulting contract was, was pretty significant when for labor, so to speak in terms of driving some of these things back in, and maybe that’s a bellwether for what to expect. I don’t know. Nevertheless, union membership, lower bargaining lower, and some people would say we’re less likely to see what we saw in the seventies.

Um, I think the other thing we have to look at, it’s just, you know, one of the rare cases are transitory private sector, government debt is massive now. Um, those that massive debt overhang is just going to stifle risk-taking innovate and growth. Um, and you know, the demand for goods and services, which ultimately keep a lid on inflation.

And that just means we’re unlikely to see the kind of same explosion, uh, inflation we saw. Um, and I’d say the other one people will look at is just any of this, you know, to the extent inflation keeps rapidly rising and outpacing aggregate growth in wages that are, um, income earning people are gonna see their real spending power decline.

And that’ll, you know, inflation will basically just have a way of choking off economic growth in that, you know, things will revert in inflation will subside on its own. So that’s kind of the transitory case. Um, the other side of the energy is. What do people think, or, or why might we have sustained elevated inflation?

And so here would come down to the main arguments on that side. It’s going to come down a lot to policy. Um, and so the argument here would be, you know, you’ve had the most expansionary government fiscal policy we’ve seen probably since world war II in terms of. Aggregate level of spending and deficits created.

Um, I mentioned 5 trillion in deficit, so you’ve had all this massive spending and then what’s more as government and Congress continues to debate more spending, right? It was the infrastructure bill that just passed the bill back better kind of social infrastructure and green energy, all these things I know.

And so on precedent levels of spending with more being debated that’s one side monetary policy then is really aided and abetted all this right. The fed has been actively buying up the new debt issuance. Yeah, I, I keep saying it’s kind of crazy to sit here. If I told somebody five years ago, inflation’s coming in at 6% year over year basis.

Monetary policy is overnight rates at zero and the fed is still buying a hundred billion dollars a month of bonds. Like I never would have envisioned that scenario. So you have this highly accommodated monetary policy. And I think some of the fears on inflation people have is that fed doesn’t seem all that concerned with inflation.

They keep talking that they believe it’s going to be transitory. You know, they’re more focused on ensuring that, um, labor recovery keeps happening and that, you know, they’re focused on things like climate change and potentially right. Adjusting the way they regulate banks for climate. You know, all these things that the argument is the Fed’s taking a science as ball, and it’s not worried enough about price stability.

Um, and there may be some truth to that. And then I think you can think about. Some of the other implications or, you know, what’s happened on policy side around, um, you know, so they’ve had this big aiding of demanding. Also some actions that arguably constrained supply. Right. Um, and so, you know, to the extent you have expanded social spending, that arguably creates a disincentive to work.

And so that may be contributing to the reductions of labor supply that we’ve seen. We’ve seen about 2 million excess retirements. You’ve also had about 2 million people aged 25 to 54 exit the labor force and haven’t come back on. Some of that’s undoubtedly due to health concerns, you know, childcare issues, as it relates to, you know, the staggered, reopening schools, all these things.

Nevertheless, you have a lot of people who have exited labor force. People will attribute some of that to, to some, um, you know, policymakers, you know, actions, you know, vaccine mandates prior to wrong. That also is causing some people to exit their jobs. And so that reduces supply. So there’s some of that stuff.

Um, global retrenchment globalization, part of that policy driven part of it, just companies wanting to make their supply chains more robust that’s happened, right? To the extent globalization helped drive costs of goods. Goods down a reversal of that, right. Should arguably push goods, prices up. Um, and so there’s a variety of some regulatory burdens would be the other thing people would heighten, which is again, just constraining supply.

So getting right or wrong. If we want to prioritize. Um, you know, Kate concern about climate change, right? Arguably that’s driving up the cost of energy and things like that in the near term. Um, other types of rules and regulations that may impact businesses that ultimately have the effect of reducing supply of goods and services, which lead to higher prices.

[00:24:53] Nicholas Olesen: Gotcha. Okay. So kind of both sides of the coin. Why we can see it either way. As we’re a wealth management firm and most of our clients come to us with the investment question, which just says, okay, I get it. I hear both sides. What do I do? Like what should investors do right now?

[00:25:09] Nicholas Ryder: So I think I’ll kind of summarize, you know, come back to my view is I think I’m preparing for the fact that inflation is likely to be with us and, you know, elevated for some time. And I’ll, I’ll say, you know, kind of baseline now expect maybe you’re one of the four to 6% per year range for a little bit, you know, a little bit of time.

Maybe that’s a couple of years. Okay. You know, we look back in the 1980s, um, after inflation came back down from, you know, it’s really high levels of the, of the, of the 70. Core CPI was about 5% a year for much of the eighties. So there is precedent for an environment like that, which is higher than what we’ve seen, not sky high, but higher than what we’ve seen inflation.

I think that wouldn’t surprise me given, you know, I tend to, you know, some of those arguments on why things are going to remain sustain, tend to resonate a little bit more with me on balance than some of the stuff on the other side of the ledger. So let’s just say we stay there and, and I’m not, again, I’m not expecting to return to 70 style inflation of 10 plus.

I also won’t rule it out though. I think there’s enough. That could cause maybe even a temporary spike to there. Maybe it’s. Single digits probability of happening. I don’t know, but let’s just say we stay in this kind of elevated range. Um, what do investors do? Right. I’ll kind of come back to, again, one of our fundamental precepts that we don’t necessarily allow macro forecast to heavily influenced what we’re doing in portfolio management, or we approach them with skepticism.

In my mind for a couple of reasons, one being most forecasts are either a repackaging, a consensus, which if it’s consensus is already known and it doesn’t have much investment value or it’s non-consensus, which rarely turns out to be correct. And then also it’s important to remember, like, I can have a view on inflation, what you do in the portfolio is that a whole nother issue.

And so getting the macro forecast being right, right is only half the battle. Then you need to. From an investment perspective of what I want to do. And that’s where even arguably it gets even harder because while we know in the long run, markets are driven by fundamentals in the short run it’s psychology sentiment, capital flows that you can get the macro, right.

But if the collective investors out there perceive it or treat it differently or react in a different way than you thought your whole thesis can be blown up. And so. Right. I, I purposely try not to get too carried away. We’re doing these things. Um, nevertheless, right? I say it’s inflation to be elevated four to six.

Let’s say for a couple of. What do we do first? Let’s remember, what are we trying to accomplish? Which is at the end of the day, when we’re investing, we’re trying to protect and grow purchasing power of a dollar. Right? And so, you know, the flip side of that inflation is being this kind of gradual erosion of the value of purchasing power.

So what I want to look for is really over the long-term. How do I invest in things? When I grow my real purchasing power net of inflation purchasing power in an inflationary. I know, you know, no silver bullet here. One thing I do want to avoid is probably intermediate long duration, fixed income assets.

So. I quality investment grade, intermediate long-term bonds. I, if I think inflation is gonna be around, I don’t want this. Um, I think I wanna keep on my fixed income allocations, much more shorter duration, you know, short maturity bonds that to the extent inflation takes, hold, or remains in hold and interest rates move up as a result of it, you know, I’m able to rapidly re-invest those kinds of maturing bonds and coupon payments into now new higher yielding.

I want to avoid things that have very long fixed cash flows that are just going to be eroded as, as inflation comes. So that’s easy. I’d say then. Yeah, I think there’s a couple of things that stand out as particularly appealing in the long run as investors in an inflationary environment and in the first.com to stocks.

Right. If we think back at their basics, what are stocks? Right? It’s an ownership interest in companies in many respects that they are real, so to speak assets, right? They earn revenue that’s in nominal dollars and they have costs that are in nominal dollars. Some of which are fixed and embedded. Right. If I have plant property equipment, these things are fixed costs that are paid for now.

There’ll be some services and all that, but yeah. There’s benefit. I’m going to earn profits and have the ability to distribute cash to my shareholders that are in nominal dollars. That will go up and down with inflation. And so I think stocks are great in terms of long-term growth generating, and that will still hold true.

You know what I think we need to be mindful of when I say stocks it’s, but if you know, inflation remains elevated and you know, it causes a growth scare or causes monetary policy to slam on the brakes and drive the economy in a recession or people just get fearful that that’s going to end up happening.

You know, stocks could sell off, um, in the short term and that’s going to be notoriously difficult to predict that that’s going to happen, but in the long run, I’ve, I’ve faith and value that stocks will will go. You know, I think some people are going to point to what you’ll often hear or look at. If you look at the historical data is, Hey, we’re at this all time kind of higher near all time, high valuation in the market.

And people will say, well, yeah, we had this inflationary environment in the seventies and valuations, you know, compressed in high inflation and remained depressed. And so people would say inflation equals bad for stocks. Um, I think we need to take that a little grain of salt because right. All this is heavily influenced by one observation.

I think we need to there’s dramatic differences between the causes of inflation now versus seventies. Um, and determining causality is going to be challenging, particularly look during the seventies, you had three recessions during that period. So it, you know, To simply make the deduction that high inflation equals bad socks is hard.

Um, it’s very possible that people look and take the same logic that I have today, which is that in the long run, I’m trying to grow my real wealth. And I want ownership interest in these companies. I think that may be partially, what’s been going on over the last year, which is people are going to things that they think can hold up and drive value in the long run.

Um, we’ll see. But I think stocks are, are, are going to be a component of it for people. I think within stocks factor tilting or active indexing, as we call it, value stocks have tended to outperform during high inflationary periods. So have high quality stocks. So companies that have. Strong financials, you know, not over, over levered balance sheets, don’t rely on a lot of external financing to persist companies that have been able to grow their earnings companies that have, you know, conservative accounting principles or higher earnings quality that speaks, um, momentum stocks.

Um, momentum’s had this propensity to, you know, stock prices have predicted companies that are able to grow earnings and that’s persisted. So I think some of these factor tilts can play a value in that. Um, add some incremental value. I think within stocks, one area you may want to be cautious about, or, you know, tilting away from some of these highly speculative growth stocks, um, in this kind of comes to the idea that a lot of these companies, right?

If I’m buying this company, that’s highly unprofitable today, based on this view that they’re going to earn a lot of money in the far out years in the future. Well, the value of that stock is, is highly, you know, uh, contingent upon long off cash flows. And so to the extent interest rates rise, that’s going to disproportionately negatively affect those types of stocks.

So I think some of those kinds of these gross speculative stocks that have done so well in recent years could come under pressure of inflation, where to, to take hold. Um, Yeah. Okay. So that’s in the stock side. Other things we’ve often talked about, um, you’re going to your kind of traditional real assets.

[00:32:56] Nicholas Olesen: Yeah. I was going to say so far, we haven’t talked about the, the asset heavy side of things, which says if inflation’s here, real estate, what we call real assets in our portfolio design. So share for those, that kind of don’t know what our thinking is there too.

[00:33:09] Nicholas Ryder: Yeah. So I think the other, other main area people may want to be looking at, um, and that we’ve increasingly had conversations about is, is real assets. And by that I’ll call it physical structures.

Um, so real estate being right, the common, when people think about, and this could be variety of types of real estate, it could be offices could be apartments, um, could even be retail, could be, you know, um, industrial kind of warehouses, right. Runs the gamut across real estate, but it’s.

What are your plot of land and, you know, a physical structure on top of it. Why does that work? Well, think about it. Replacement cost rationale would be the first, which is to the extent inflation goes. Um, it will just cost more and more to replace those existing structures, which means the existing ones will go up in value.

Um, kind of simple as that income growth being the other component is right. If I own an office building and I have tenants paying my rent, paying rent over time, rents will increase as inflation goes up too. So there’s this kind of real structure to these things, which has really. Yeah, it’ll differ a little bit, but infrastructure assets, these could be things like data centers, cell towers, um, airports, toll roads, ports, um, rail, railroad rail, right?

Uh, rail stations and tracks all these things, right? Infrastructure assets, same dynamic will be at play, which is they’ll cost more to build, but they also, the income that Janet gets generated from them will go up as, as time passes to, um, Farmland Timberland or to other areas. We look at same dynamics playing at play there.

Um, we gotta look at all these they’re kind of pro inflationary assets, um, stand to at least preserve and then have you that op op you know, ability to grow, purchasing power over time. So those are some other areas where when you think about within a portfolio, Maybe it’s lightening up on kind of your traditional fixed income and going into these hybrid securities is kind of how I think about real estate, um, infrastructure, farmland, Timberland, all these things.

They kind of sit somewhere between stocks and bonds on the risk spectrum. And so, um, you know, potentially having conversations about moving into some of those that have the ability to generate returns that are in excess of inflation, um, without necessarily the full level of volatility risks, that’s that’s, you know, um, in the stock market,

[00:35:29] Nicholas Olesen: No, that’s really helpful. And I think, um, we talked about it, but we’ll do a separate podcast that kind of goes through our thinking on portfolio design. Because every time we’ve talked about it, with prospective clients or current clients, it helps them understand why we talk about these buckets and kind of themselves categorize it as what, uh, what am I willing to take? What do I need in reserves? And then what does this kind of middle risk of our growth bucket, if you will.

So I’m teasing that one for a future episode.

Anything else that we should be mindful of or share, as we’re wrapping up here?

[00:35:55] Nicholas Ryder: Yeah, think the other things you’ll hear about which, which may or may not play a role in a portfolio, I think there’s considerations people know. You’ll hear an inflationary environment, commodities could be energy, agricultural, precious metals.

Theoretically, right, all those should maintain value, uh, in an inflationary environment, you know, they’re real assets in that front. You get to some issues of implementation, you know, buying physical versus implementing via future. There’s also not a ton of rationale necessarily to believe, like why should these things grow my real purchasing value? Um, so, but they may be able to preserve purchasing value in the commodities space. Precious metals would be the, you know, the kind of sub-sector of that gold would be the prime example there, same story as commodities broadly. I’m not telling the net rationale necessarily as to why it should grow your purchasing power, but theoretically, you know, should be able to preserve it in a, you know, if the dollar gets debased.

[00:36:53] Nicholas Olesen: So then I’ll ask you the one that’s going to hit, it’s like lighting gasoline, which is crypto. How does that fit? is that kind of this run-up that we’ve found in price?

[00:37:02] Nicholas Ryder: Yeah. I mean, I think you’ve seen in the last year, it’s just been this run-up and everything. It’s kind of the, everything rally. Right. Um, and I think that’s the other part of inflation, right? Money system got flooded with money. Part of the runaway inflation was goods and services. The other one was in asset values, right? Yeah. People bought stocks, they bought bonds, they bought commodities, they bought crypto assets, they bought real estate. Right. All of these things saw their value go up because there was cash flooding the system.

Um, I think there’s some merit to, you know, select cryptocurrencies.

I think it’s a picking and choosing being right on this. Bitcoin would be the one that stands out to me. Right. Bitcoin has these features of so-called digital gold. Um, it’s the only asset that’s got absolute scarcity. And by that, written into the code of Bitcoin. There will only ever be 21 million of them outstanding. Um, that’s as it there’s scarcity to that, to the extent, you know, somebody is worried about a continued debasement of Fiat currencies, like the U S dollar, the Euro, the Yen, whatever it be. Right. There could be refugee in Bitcoin. Um, Bitcoin is, you know, kind of emerging as this store of wealth relative to historically gold has played that role. I think the two can be highly complimentary to one another.

Some of the other ones, um, it’s going to be asset by asset, right. You know, you’ve got some of these, um, uh, tokens or currencies that, that, that support blockchain, that back these blockchains that could support functions like decentralized finance, other applicants.

You know. I kind of look at those as much of kind of startup technology businesses that could add value in you. You need to understand what’s the technology. This is token is meant to support in what’s the prospect for use on that. And then the dynamic of how much do I think other people are going to come in demand for these certainly, Hey, there’s opportunities there that you get into a very nuanced discussion of which one’s more the attention, which ones aren’t, because I think there are there’s multiple thousands upon thousands of crypto assets out there. And you see these, you know, the funny spikes that happen in these massive run-ups that happen in certain ones and they gain a ton of attention and popularity and, you know, left on is the, the countless thousands that are going to zero or do absolutely nothing.

And so, um, I think with that space selection implementation, right. You know, patients or to merit are credible local, which is you might have the right long-term view on things, but the swings can be pretty wild for sure. So.

[00:39:34] Nicholas Olesen: Good. No, this was great. I really appreciate the time. I think that’s a good primer on how we view it, what the implications are and, the so what of inflation, as we’re all seeing these headlines? That’s all I got, anything else?

[00:39:46] Nicholas Ryder: No, we love talking about this concept and, you know, our thinking will continue to evolve as, as the dynamics evolve and, you know, it’s, it’s, um, it’s certainly an interesting time and trying to figure out the right way to, to approach this for our clients in the long run.

[00:40:03] Nicholas Olesen: Yeah. Look, I think it’s legitimately the couple of trillion dollar question, what does this do to asset prices in all contexts. I appreciate it. We’re going to wrap it up there. We thank everybody for their time. I know it’s incredibly valuable. So we thank you guys. And, uh, we will record another one soon.All right.