19 Jun The Stock Market is not the Economy

As the stock market has soared higher since its late-March lows, countless pundits and talking heads on the financial media have continued to express shock and bewilderment about how the market can be in the midst of a historical rally when the economy is experiencing its worst economic contraction since the Great Depression as evidenced by the continued stream of abysmal economic data releases including those revealing that unemployment rolls have climbed into the tens of millions. While the notion that the stock market and the economy are tightly linked certainly appeals to intuition, logic suggests, and empirical evidence demonstrates, that the contemporaneous link is actually effectively nonexistent.

Starting with the logical case for why the stock market and the economy may not be as closely linked as is often assumed, I see three primary factors that undermine the link:

First, stocks derive their value from earnings, not economic growth, not from employment and not from any other macroeconomic indicator. Earnings of individual companies and the market in aggregate can and do grow at different rates and in different cycles than the broader economy. Beyond what happens in the immediate, near term, it’s also important to recognize that stocks derive the preponderance of their value from their very long-term earnings potential (a topic which I covered in a previous post). Thus, even a significant short-term hit to earnings could have a negligible effect the intrinsic value of an individual company or the market aggregate.

Second, the domestic economy in which stocks operate or domiciled is not the only one from which they derive their revenue, expenses and ultimately earnings. To the extent that companies operate beyond just their home companies, the link between the economy and the stock market is further weakened.

Third, and arguably most importantly, the stock market is forward looking. Markets are information processing mechanisms that enable short-term traders and long-term investors alike to express their views on the prospects of individual companies via buying and selling activity that drives the collective wisdom of all participants into securities prices. While this process is certainly subject to periodic bouts of error and noise, the fact that markets operate to embed predictions about the future, not the past, into market prices further weakens the link between the economy today and the stock market.

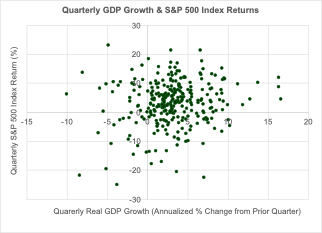

Turning now to the empirical data, the chart below plots the relationship between quarterly GDP growth and the stock market’s returns. A quick examination of the chart plainly demonstrates that there is no statistical relationship between contemporaneous real GDP growth and quarterly stock market performance.

The implication of this is that all of the handwringing and obsession over macroeconomic figures measuring what happened in March, April and May is of little use for serious long-term investors. What matters is how the future will unfold relative to the expectations currently embedded in security prices. To the extent one believes markets are pricing in a too optimistic or too pessimistic outlook for the future relative to your expectations, opportunities exist for investors to position themselves accordingly. However, given the well-documented underperformance of active managers in aggregate against passive market indexes, assuming the market has it completely wrong is no doubt a risky proposition which is why I routinely advocate for erring on the side of caution when sizing active bets within a portfolio

Sources:

S&P 500 Index Returns from Morningstar Direct.

Quarterly Real GDP Growth from St. Louis Federal Reserve Bank, FRED.

Important Disclosures

Kathmere Capital Management (Kathmere) is an investment adviser registered under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply any level of skill or training. The information presented in the material is general in nature and is not designed to address your investment objectives, financial situation or particular needs. Prior to making any investment decision, you should assess, or seek advice from a professional regarding whether any particular transaction is relevant or appropriate to your individual circumstances. This material is not intended to replace the advice of a qualified tax advisor, attorney, or accountant. Consultation with the appropriate professional should be done before any financial commitments regarding the issues related to the situation are made.

The opinions expressed herein are those of Kathmere and may not actually come to pass. This information is current as of the date of this material and is subject to change at any time, based on market and other conditions. Although taken from reliable sources, Kathmere cannot guarantee the accuracy of the information received from third parties.

An index is a portfolio of specific securities, the performance of which is often used as a benchmark in judging the relative performance to certain asset classes. Index performance used throughout is intended to illustrate historical market trends and performance. Indexes are managed and do not incur investment management fees. An investor is unable to invest in an index. Their performance does not reflect the expenses associated with the management of an actual portfolio. No strategy assures success or protects against loss. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk. All investing involves risk including loss of principal. Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market. Past performance is no guarantee of future results.

S&P 500: Standard & Poor’s (S&P) 500 Index. The S&P 500 Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad U.S. economy through changes in the aggregate market value of 500 stocks representing all major industries.